Lumen Technologies (LUMN) Deep Dive

The Market is Pricing a Dying Telecom. It’s Becoming an AI Toll Road

Section 1) The bet in a nutshell

What it is: LUMN owns the premier U.S. long-haul fiber network - an irreplaceable, decades-in-the-making asset the market still values as a melting ice cube.

What the market thinks: A complex, over-levered, structurally declining telecom with a history of value destruction.

What I think: That same asset is becoming the physical backbone for AI/cloud data movement + the balance sheet has been de-risked and simplified + revenue and EBITDA are inflecting from decline to growth. None of this is in the price.

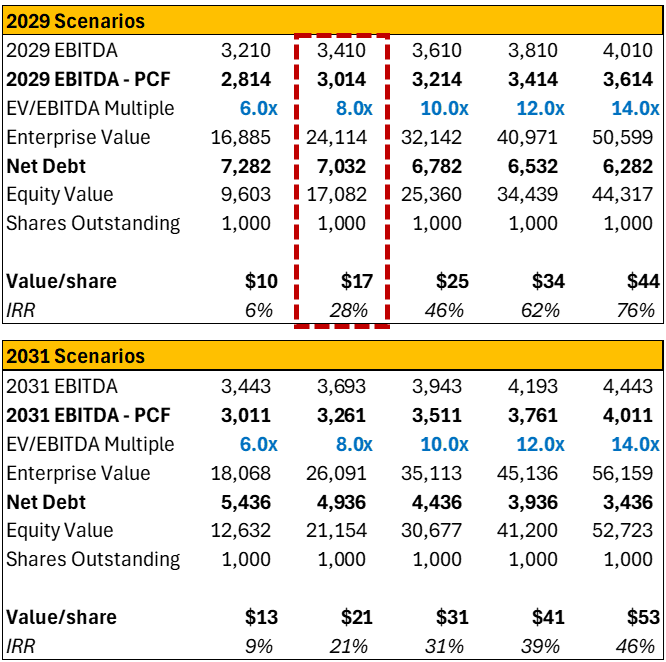

What you get paid/the skew: ~$17 base case (8x 2029 cash EBITDA) + further upside skew (~$25–44 if the turnaround re-rates the multiple to 10-14x), against ~$8 today. Downside is cushioned by an asset base worth multiples of the current enterprise value and the 2029 bear case (6x EBITDA and no inflection) lands roughly at today’s price.

· Very wide range of outcomes, but the skew is not symmetric. On 2029 #s, valuation range of $10-44 (IRR of 6% even in bear case). On 2031 #s, $13-53/share valuation range with a 9% IRR in bear case.

Section 2) What is LUMN, and why it’s neglected and mispriced

Note: See Glossary for further description if unfamiliar with Lumen/industry jargon.

LUMN has effectively become two businesses stacked on top of each other:

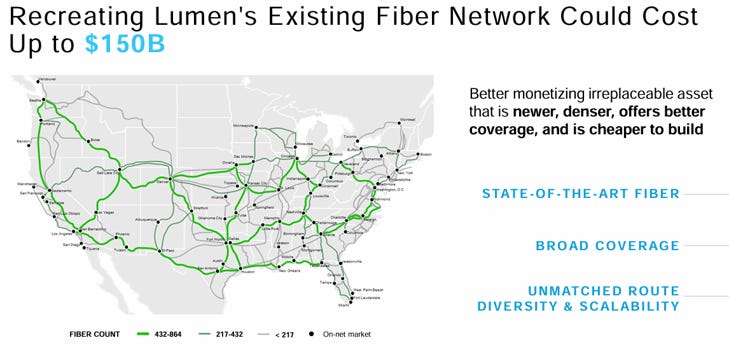

A physical network: more than 340,000 route miles of intercity fiber and conduit, ~160,000 on-net buildings, and the largest 400G footprint in the U.S. (~78–90K route miles across 70+ markets). The crown jewel is the Level 3 intercity network - “5–10 lane interstate highways” versus the “driveways and city streets” of consumer-focused carriers such as T/VZ. The Qwest assets are mostly legacy copper in run-off.

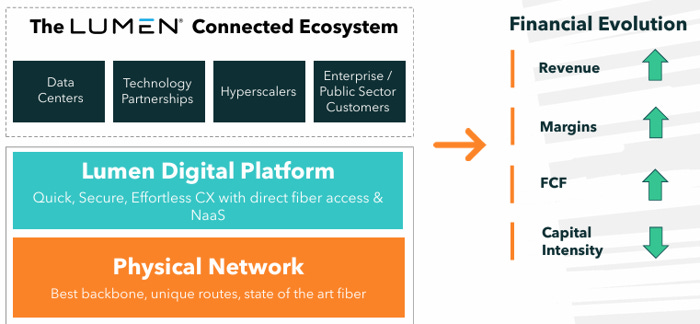

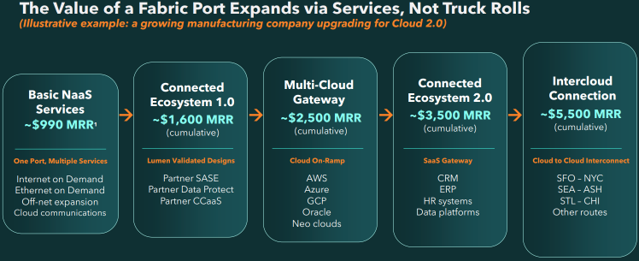

A software/services layer being built on top of it: most importantly NaaS (Network-as-a-Service), a programmable, API-driven way to provision connectivity on demand. NaaS is to connectivity what AWS is to compute: incremental services run over an installed fabric port without new hardware, so they can carry software-like margins. The fabric port also allows customers to join off-network from their location. LUMN owning the physical network provides a substantial competitive advantage over pure-play NaaS companies and allows LUMN to get owners economics.

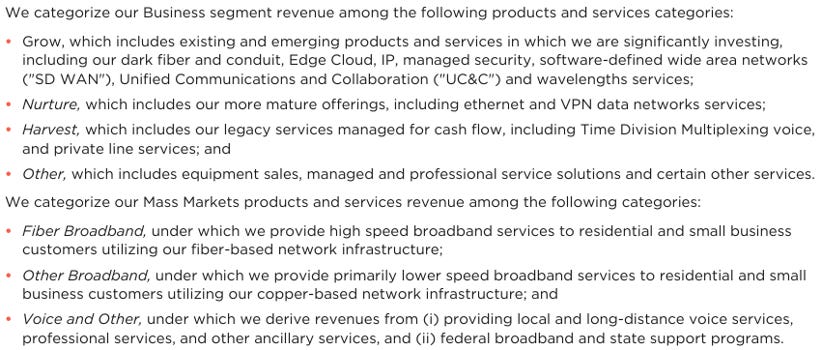

Brief Overview

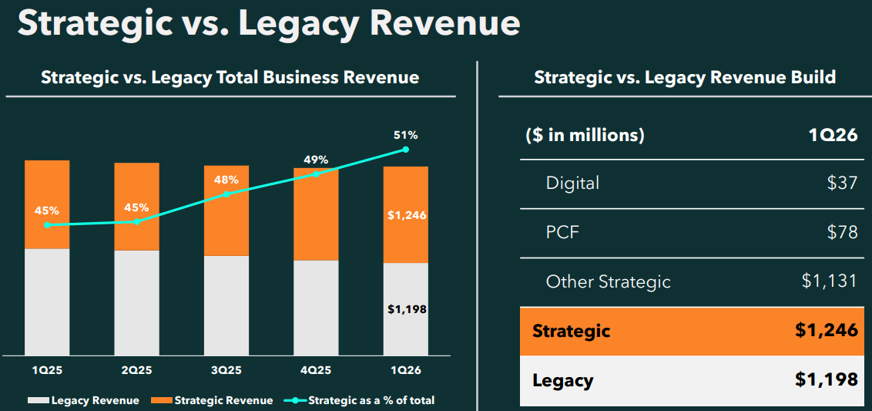

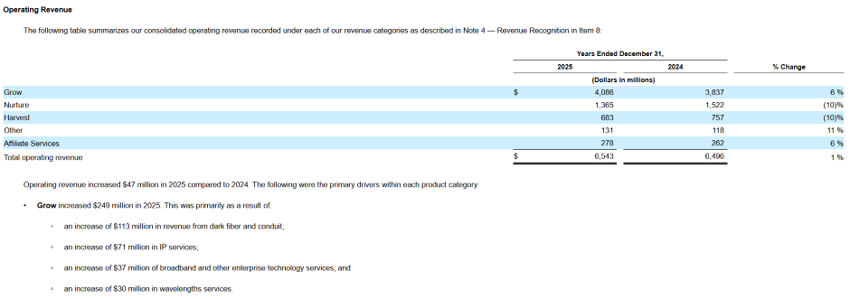

After the early-2026 sale of the fiber-to-the-home (FTTH) business to AT&T, the Business segment is over 80% of revenue, with a fast-shrinking legacy copper tail. Within Business, reporting is now Strategic (the growth engine) versus Legacy (run-off). Strategic (~now larger part of mix than Legacy) is the growing enterprise/Level 3 business including fiber, waves, IP, and security. Customers are mainly large enterprises and hyperscalers which represent the highest growth/largest sub-segment. Mid-market and public sector represent a large portion of the remaining. Legacy is the declining copper/voice book.

Below is a bridge from the old segments (including description) to new (as of Feb 2026 Analyst Day), noting Fiber Broadband is no longer part of the mix.

As of Q1/26 we are already seeing early signs of the mix shift making an impact. NA business strategic revenue as of the most recent Q1/26 results grew 5% q-q and 9% y-y (8% y/y growth average last 5 quarters, and large enterprise strategic grew 16% y/y. Revenue declines are improving.

Why it’s mispriced: The old bull case “the fiber is worth $50 billion+” is stale, and a jaded reader’s eyes glaze at it, because that argument has been made the entire way down to a single-digit stock. So I’m not leading with it. The actual misperception is this: the market is still extrapolating legacy decline, while the business mix has already crossed the point where growth in the strategic/AI-levered segments outweighs the legacy run-off. Strategic passed 50% of Business revenue for the first time in Q1/26. Business revenue is guided to inflect to growth by 2028, with EBITDA inflecting in 2026. The Street has watched a decade of telecom declines and is pricing continuation; the company’s own segment math says the curve bends.

The gap exists for good structural reasons — the systemic bottlenecks that create opportunity:

Coverage neglect: Of 14 sell-side ratings, 2 are sells and only 1 is a buy. Analysts spend their time on Verizon and AT&T; LUMN is the afterthought ticker on the page.

Complexity: Three reporting entities (Qwest, Level 3, Lumen parent), many sub-segments with wildly different growth rates, several divestitures (LATAM, EMEA, 20-state ILEC businesses sold for ~$12B in total) and, until recently, a capital structure spanning super-priority through unsecured across three separate silos. Complexity itself is a discount.

Scar tissue: The CenturyLink/Level 3 merger failed, the dividend was cut, and the company executed one of the largest out-of-court debt restructurings in U.S. history in early 2024. Survivors of that don’t extend benefit of the doubt.

Short reports (Kerrisdale and others) reinforcing the bear narrative: addressed head-on below.

The skepticism is the edge here, not a reason to pass. There are many minds to change, and the catalysts that change them are identifiable over the medium-term.

Consensus models business revenue inflecting in 2030 and 2029 EBITDA of ~$3.13B; I underwrite the inflection a year earlier at ~$3.6B 2029 EBITDA, a ~15% gap driven almost entirely by Strategic mix shift/NaaS scaling/PCF EBITDA + $1B of cost cutting offset by continued legacy declines (not betting this changes).

Section 3) The structural dislocation - why now

Two things have changed that the price hasn’t caught up to.

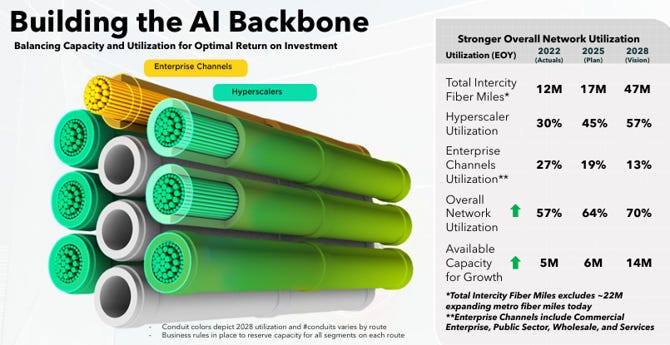

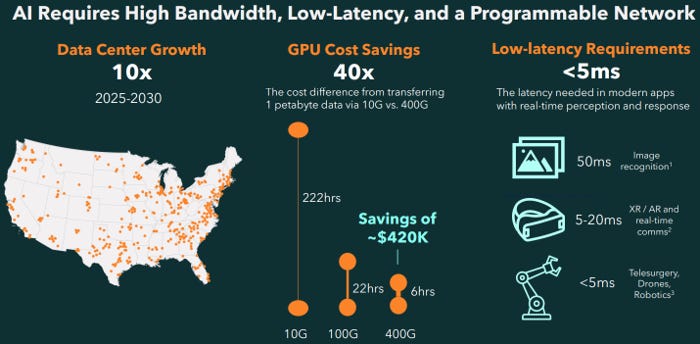

First, demand for the asset has structurally re-rated. The network was built over decades for voice and enterprise data. AI/cloud has turned high-bandwidth, low-latency, point-to-point fiber into a scarce input. Data center spend is expected to be >$500B in 2026, with trillions expected over the next decade; AI data movement is estimated to grow more than 10x from 2023–2030, needing hundreds of millions of new fiber miles. This is a step-change in the ROI on a pre-existing, hard-to-replicate asset, not a new asset that has to be built and proven.

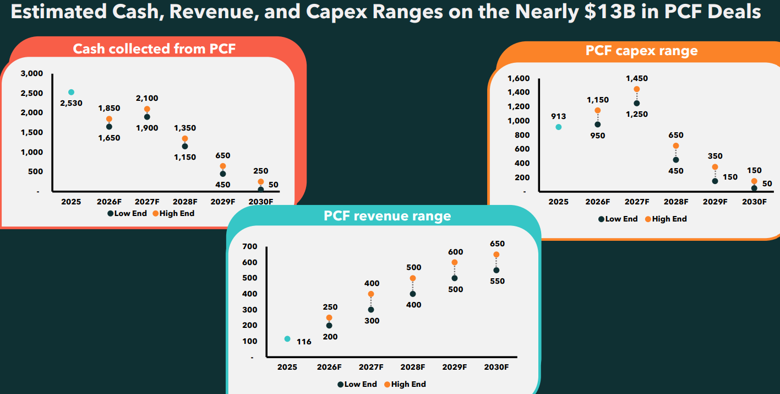

The clearest evidence is the PCF (Private Connectivity Fabric) wins: roughly $13B of deals signed since August 2024 (notably with Microsoft/hyperscalers), structured with large near-term cash prepayments, mostly by lighting empty conduit - monetizing a tremendous amount of existing capacity at high incremental margins.

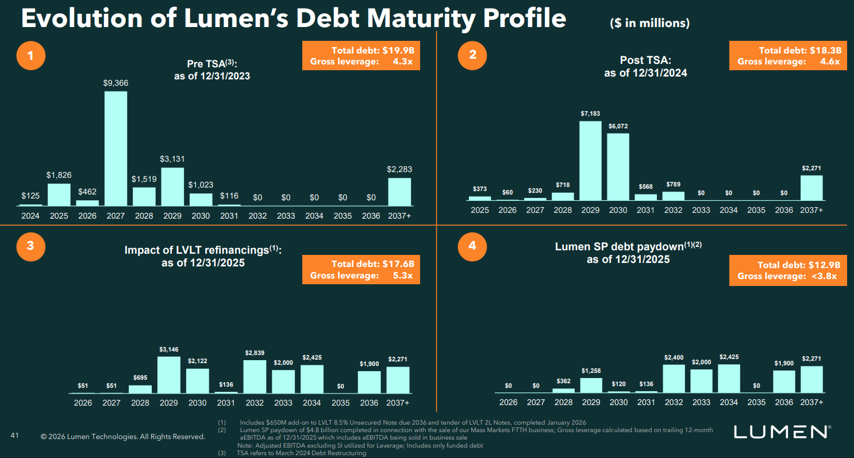

Second, the balance sheet was de-risked and simplified (Appendix). After the ~$5.75B FTTH sale to AT&T, LUMN repaid ~$4.8B of super-priority debt, cut net leverage by ~1.5 turns to below 4x, and removed ~$1B of annual capex. Combined with a year of Level 3 refinancings, run-rate cash interest falls from ~$1.2B toward ~$700M. Recent debt exchanges brought the Qwest notes under the Lumen parent guarantee, collapsing three credit silos toward one. Maturities have also been pushed out.

That second point is an under-appreciated re-rating catalyst, not just a credit event. Part of the discount here is a complexity-and-distress discount, and it is actively being dismantled. A simpler, lower-leverage structure widens the pool of equity investors who can own the name.

The growth drivers the Street under-models:

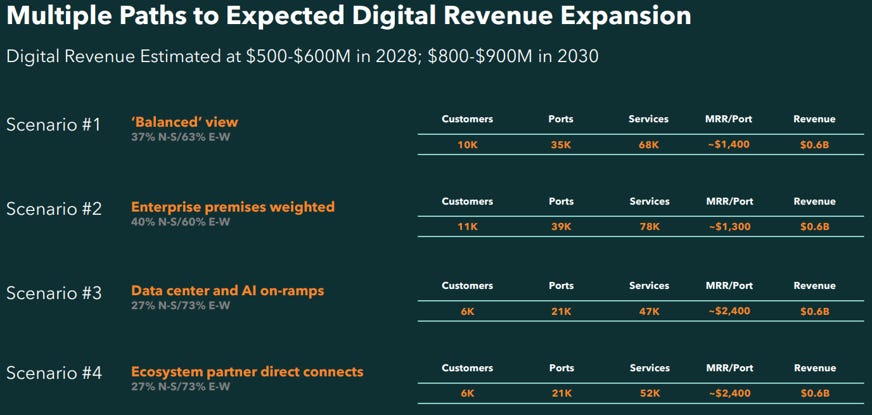

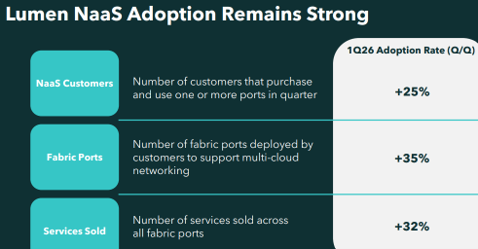

NaaS - software margins on a physical moat. NaaS was ~14% of LUMN’s ~$116M of 2025 digital revenue which in total grew 36% y/y, with customer count/current metrics indicating rapid growth, as shown in the Appendix (>2,500 customers, >3,800 active ports). It’s the swing factor in management’s $500–600M 2028 digital-revenue target. Because additional services sell over an existing fabric port “via services, not truck rolls,” NaaS is margin-accretive. If it J-curves, this drives EBITDA well above base case. The TAM penetration implied is LSD%.

PCF - a free option. The ~$13B signed nets ~$1.8B of after-tax cash in 2026–2030. My numbers assume no further PCF wins, yet each incremental $1B is ~+$0.25/share of NPV, so the pipeline of potential further enterprise/cloud/datacenter demand is upside I’m not paying for. (Caveat: future PCF may increasingly need new conduit rather than overpulls, which is lower-margin and higher-risk, and Zayo competition could rise. I treat new PCF as optionality, not base case.)

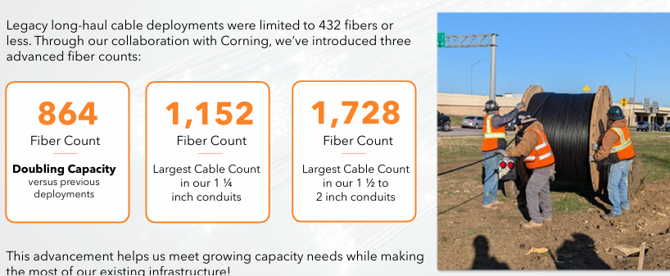

Platform partnerships. AWS on Lumen Digital, Palantir integrating data with LUMN’s network, and the Corning fiber-density partnership (enabling up to a ~4x increase in fiber miles 2022–2028 at low incremental cost) deepen the moat and the services attach rate. Digital services also come in at lower churn and higher margin.

· Alkira Acquisition (adds ~0.2x to EV/EBITDA): at Q1/26, for ~$475M, LUMN will save $100-200M of CAPEX and several years of time in effectively a buy vs build decision. Alkira represents a cloud-native NaaS control pane for a single digital platform. With immaterial revenues today, hard to judge this deal but management has earned the benefit of the doubt based on execution thus far.

I don’t need the full ~$58B data center/cloud/hyperscaler connectivity TAM management points to. I need the mix shift to do what the segment math already implies – Revenue Growth section below.

Section 4) Valuation and margin of safety

Ex-PCF (~$500M) and the re-classified AT&T proceeds ($729M), adjusted FCF for FY26 of ~$800M is a ~10% levered FCF yield. Longer-term, I expect >$1B with upside if NaaS scales faster than expected.

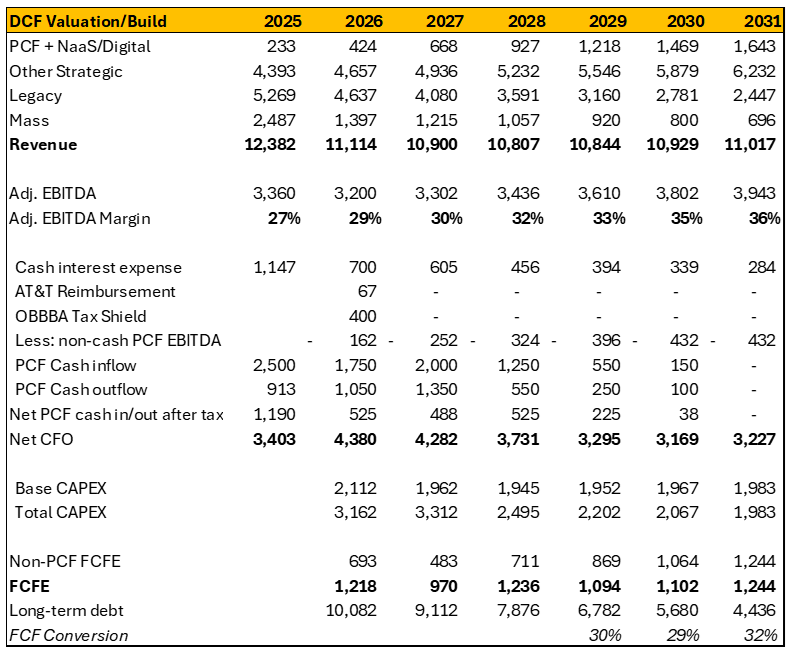

Below is my base case financials build and key assumptions explained:

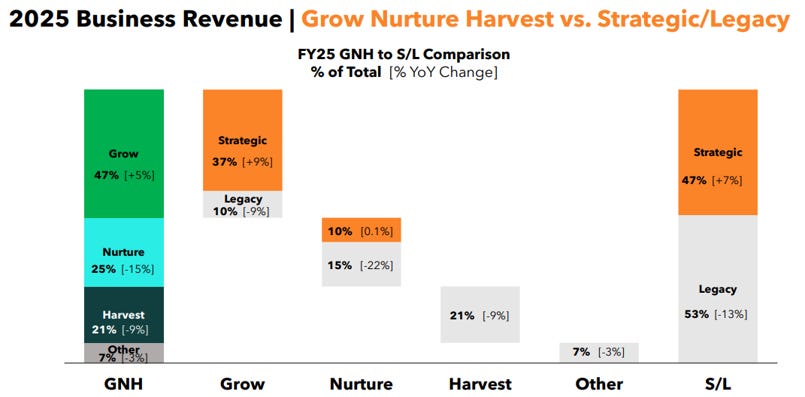

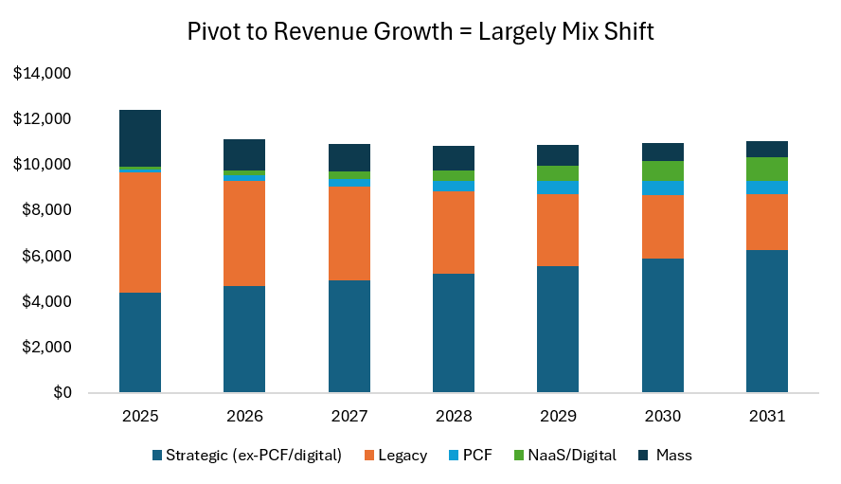

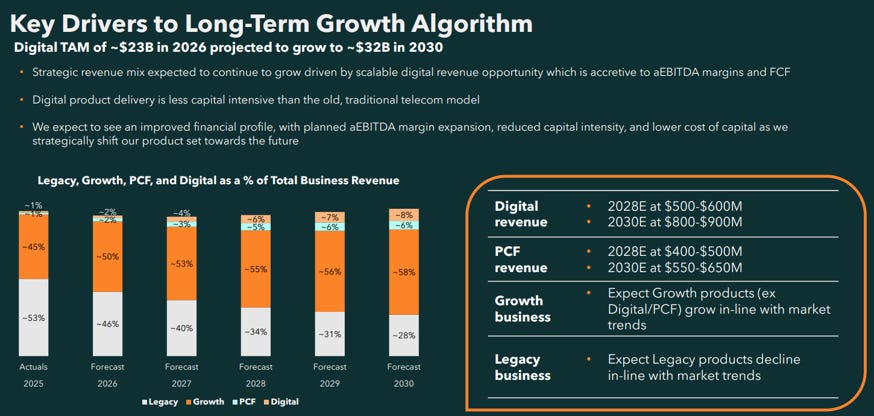

Revenue Growth: Following the FTTH sale to AT&T in early 2026, the graph below shows the resulting go-forward mix shift dynamic, with Strategic revenues going from ~1/2% of business revenues to >60% by 2031 and digital going from ~2% to ~16%. I assume for Strategic/Legacy/Mass revenues a growth rate of 6%/-12%/-13%, roughly in-line with historical and guidance after adjusting for divestitures. The PCF and Digital revenue is in-line with management guidance. Please see Appendix for a bridge from old Grow/Nurture/Harvest segments as well as a description of the services in each.

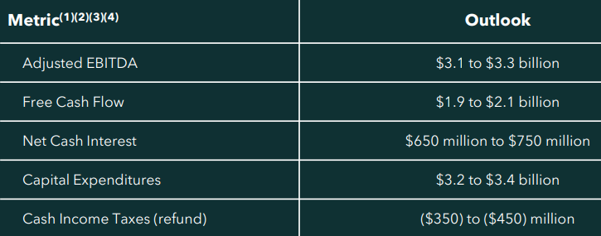

2026 #s: modelled consistent with guidance (Appendix).

EBITDA margins: 36% by 2031. Bridge from 27% to 36% includes ~5% from PCF ($600M revenue at ~80% margin) + $1B cost cutting + $1B digital growth – legacy/mass declines of $2.9B at 50% decremental margins. Worth noting NaaS and other strategic revenues carry high incremental margins (e.g. waves is 75%+).

PCF: no further PCF assumed ($13B cumulative). Consistent with analyst day guidance on cadence (Appendix) and assumed 25% cash taxes. Lump sum payments finish in 2030 and revenue/EBITDA of ~$600M/$480M with only 10% of EBITDA being cash. Cumulative FCF from 2026-2030 of ~$1.8B after-tax.

Digital: from $116M to $1B by 2031, slightly below guidance in 2028 ($477M) and in-line with 2030 guide. Current growth rate according to management is 36%, with NaaS likely growing faster right now given solid KPIs (~14% of digital is NaaS today).

CAPEX: moderating to 17-19% intensity post PCF builds.

Taxes/NWC/debt/interest/taxes/dilution: I assumed all FCFE reduces net debt as a conservative proxy for capital allocation which drives leverage + interest expense below guidance. In reality, at 3x leverage LUMN could pivot to buybacks which is upside I am not crediting. 5-6% cost of debt on improved credit ratings, nominal taxes (NOL carryforwards/negative net income), nominal NWC/dilution.

Note: millions of USD unless otherwise stated.

Scenario Analysis

This is the section I most want a professional reader to trust, so I’m explicit about methodology.

The trap I’m avoiding: PCF is economically a prepaid capacity contract: cash arrives up front, but revenue and EBITDA are recognized over the life of the deal. If you (a) capitalize reported EBITDA at an EV/EBITDA multiple and (b) separately count the PCF cash, you double-count PCF. The fix is to be consistent about cash:

I value the ongoing business on cash EBITDA = reported Adj. EBITDA - the non-cash PCF EBITDA being amortized that year. I capture the PCF cash through the net-debt walk and let the prepaid cash pay down debt rather than adding it as a separate capitalized line. PCF is then counted exactly once, on a cash basis.

Capital allocation: the most conservative place is debt paydown (a guaranteed return at the cost of debt); buybacks at ~$8/share would be more accretive, so paydown is the conservative base and buybacks are noted upside.

I treat 8–10x as reasonable-to-conservative for what’s becoming the premier AI-grade fiber network with growing/accelerating revenue and moderate leverage, against a 5-year LUMN average forward multiple of ~5.5x (4–8x range) earned as a declining telecom. The re-rating from “declining telecom” to “growing AI infrastructure” is the largest value driver and the one with the widest error bars.

· Even at 6x and minimal debt paydown from here, the risk of capital impairment is minimal.

· It is worth noting ~12-14x EBITDA is where quality long-haul fiber assets such as Zayo and growing telecoms like Cogent pre-issues have traded.

While $3.6B of EBITDA also screens conservative (~flat vs today ex-PCF), higher than expected growth of digital services (e.g. NaaS) at high incremental margins could lead to a significantly higher EBITDA/FCF level and multiple (I attempt to capture this in the right tail). I anchor my base case ($17/share) to an EBITDA $200M below my model and the low end of my fair multiple range (8x).

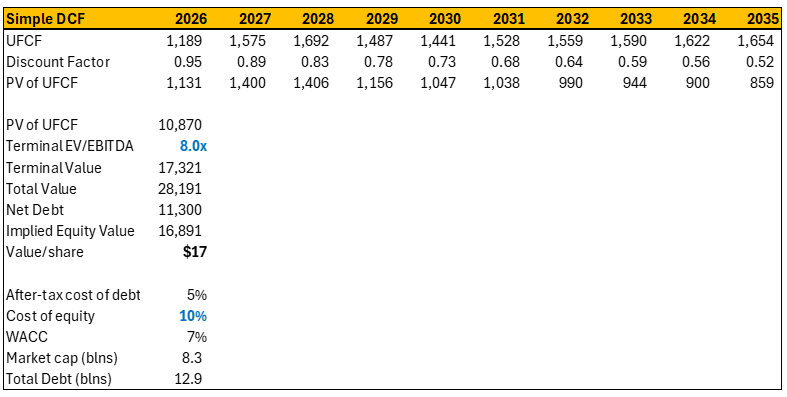

Cross-check 1 – DCF: A simple DCF (cost of equity 10%, terminal 8x on non-PCF EBITDA / ~3% EBITDA growth from 2031-2035 / 2% FCF growth from 2031-2035). 2) supports ~$17/share. This is in-line with my base case 2029 scenario above at 8x EBITDA.

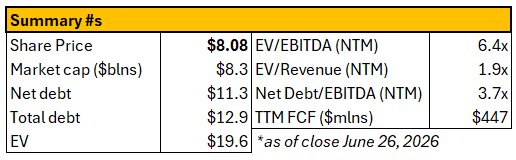

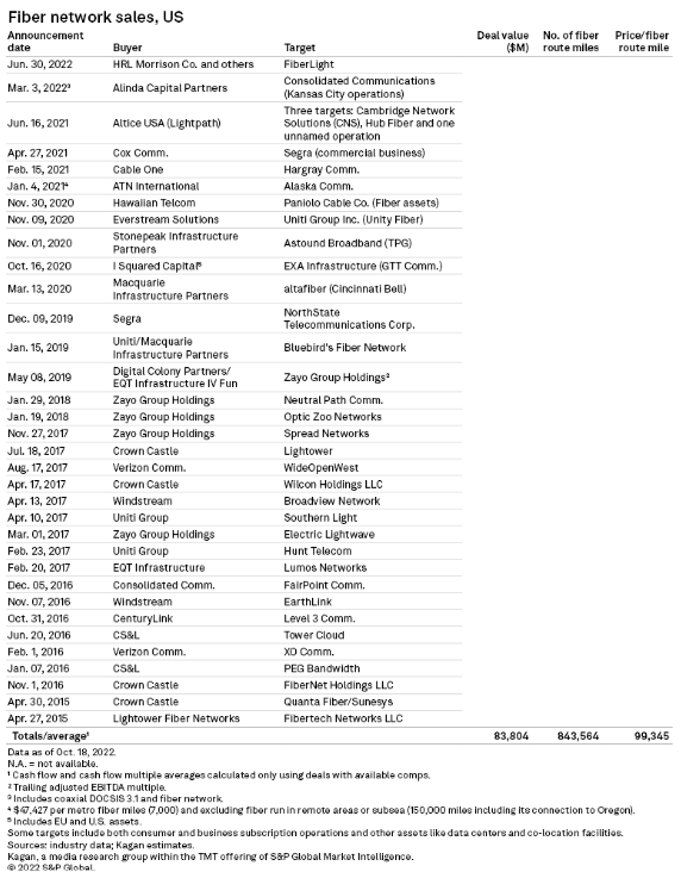

Cross-check 2 - asset value (Appendix): Per S&P, U.S. fiber sold for an average $99,345 per route mile across ~$84B of 2015–2022 deals (~11x cash flow). At that average, LUMN’s ~340K route miles imply ~$34B of asset value or roughly $23/share post-FTTH, versus an ~$8 stock and ~$19.6B EV. Replacement cost is higher (management cites up to ~$150B; aerial builds run $40–60K/mile, underground $50–120K+) and LUMN’s fiber network could be considered “too big to fail”.

· Reference deals: Zayo at ~$14B / ~12x (~130K route miles, mostly long-haul like LUMN); Level 3 originally at ~12x; Frontier at ~$111K/route mile; Crown Castle’s less dense metro fiber at ~$50K/route mile / ~7.2x in effectively a forced sale. I do not believe LUMN is a likely M&A target unless valuation stays depressed for a long time.

Why the equity (not the bonds): The credit has already re-rated (upgrades, lower coupons, maturities pushed past 2030), so much of the balance-sheet-fix return has been earned by bondholders. The remaining asymmetry, operational inflection, multiple re-rating, and deleveraging accrues to equity. With net leverage below 4x and falling, each turn of EBITDA the market pays above ~5x assuming 3x leverage is ~$3.5–4/share of upside to equity. The equity is the levered call on the re-rating.

Section 5) Catalysts and risks

Catalysts:

1) EBITDA inflection in 2026: the first proof point.

2) Business revenue inflection in 2028: the catalyst the market is most skeptical of, and therefore the most powerful for changing minds. A NaaS J-curve of growth at high incremental margins is upside to it, not a requirement. Total revenue is guided to inflect in 2029.

3) Capital returns / further deleveraging: ~$1.8B of PCF cash and >$4B of deployable FCF over four years against a 3–3.5x leverage target; buybacks at a single-digit price would be highly accretive.

4) Further AI-demand catalysts: incremental PCF wins (~$1B ≈ +$0.25/share NPV), new hyperscaler/partner deals, NaaS milestones.

Risks: The bear case, steelmanned and rebutted. The shorts (e.g. Kerrisdale) aren’t stupid, and ignoring them isn’t credible:

1) “It’s been a $50B asset all the way down to ~$1 - a value trap.” Fair, which is why asset value is not the core driver of my thesis. What’s different now is a demand-side inflection showing up in signed contracts and reported segment growth, plus a balance sheet that no longer forces distressed decisions. The catalyst is the change in cash flows, not a re-discovery of the map.

2) “Fiber oversupply pressures transport/wave pricing.” The most legitimate risk.

Response: differentiation is increasingly density, latency, 400G footprint, and direct hyperscaler access - not commodity price (given high GPU cost). The NaaS layer deliberately moves revenue off per-bit pricing; and the base case needs only the guided mix shift, not pricing heroics. If oversupply is worse, it shows up as a lower multiple and slower NaaS - captured in the bear column, where you still roughly hold today’s price.

3) “Legacy decline outruns Strategic growth; the inflection never comes.” The core bear EBITDA case. But the inflection is mix, not one heroic line: Strategic is already >50% of Business revenue, growing ~8% on a 5-quarter average (large-enterprise Strategic +16% y/y in Q1/26), while Legacy shrinks off a smaller base.

4) “Execution/capex risk - management overspends chasing growth.” Management (in place since 2022, incentivized on TSR/EBITDA) has delivered the divestitures, restructuring, and refinancings as promised, with capex guided down to 17–19% intensity ex-PCF. I’d rather own this with the bar low than after the inflection is proven.

5) Residual risks: complexity; execution and capex overruns; accelerating legacy declines or share loss (e.g., to Cogent); fiber oversupply and transport pricing pressure; PCF mix drifting toward lower-margin new-build; Zayo competition. These are real and they’re also why the name is cheap, sentiment is washed out, and the 2028/29 guidance doesn’t require heroics. The asset floor and the deleveraging let me be wrong on timing without being wrong on capital.

Note: the author holds a long position in the security analyzed.

Blindspot Value Disclaimer: Blindspot Value is an independent research publication for informational and educational purposes only. Nothing contained herein constitutes investment, financial, legal, or tax advice, or a solicitation to buy or sell any securities. Capital structures, cyclical industries, and special situations carry significant risk. Always conduct your own independent due diligence or consult a registered financial advisor before making investment decisions. The author may hold positions in, or execute transactions involving the securities discussed.

Glossary/Key Terms

Dark Fiber: Strands of optical fiber that are laid out but remain “unlit” or inactive, not actively transmitting data. Lumen leases this infrastructure to organizations, which then manage their own network traffic and light the fiber themselves to tailor connectivity to their specific needs.

Fiber Conduit: The protective piping or pathway installed underground that houses fiber optic cables. Lumen uses advanced fiber and cable systems that allow fitting more fiber into existing conduit to expand capacity efficiently.

Network as a Service (NaaS): A cloud-based model where customers use third-party services to run their network operations on a subscription basis, rather than owning, building, or maintaining their own physical network infrastructure. This allows for on-demand ordering, scaling, and management of network services via digital platforms and APIs.

Private Connectivity Fabric (PCF): A custom network architecture offered by Lumen that gives businesses total control over their connectivity, allowing them to build a private, high-performance network using dark fiber, waves, ethernet, and IPVPN. It is designed for demanding workloads, such as AI, requiring low latency and high scalability.

Waves (Wavelengths) – a $500M+ business for LUMN: Refers to Lumen Wavelengths services, which offer dedicated, point-to-point Layer 1 connectivity. Unlike shared or packet-based services, waves provide fast data transmission, low latency, and optimized security, ideal for high-throughput applications.

Section 6) Appendix

Lumen description/context/guidance: Lumen is evolving from a traditional telecom provider to a tech platform that integrates high speed fiber networking, edge computing, and automated digital capabilities to power the data intensive demands of the AI era. LUMN leverages massive fiber footprint to move and process data with extremely low latency. The Level 3 network would take years and tens of billions of capital to replicate, the structural shift in the demand for these assets driven by AI/cloud should effectively result in a step-change to the ROI on these fiber assets. The mix shift can be seen in long-term guidance below.

FY26 Guidance

LT Guidance

Network Expansion

Value of network

PCF Cash Inflows (before tax – I assumed a 25% cash tax rate) – net is $1.8B from 26-30.

NaaS Snip & Impacts – Current Metrics Look Strong: Analyst Forum 2025

LUMN’s offerings will increasingly not depend on price

What’s a mile of fiber worth? (Source: S&P Global)

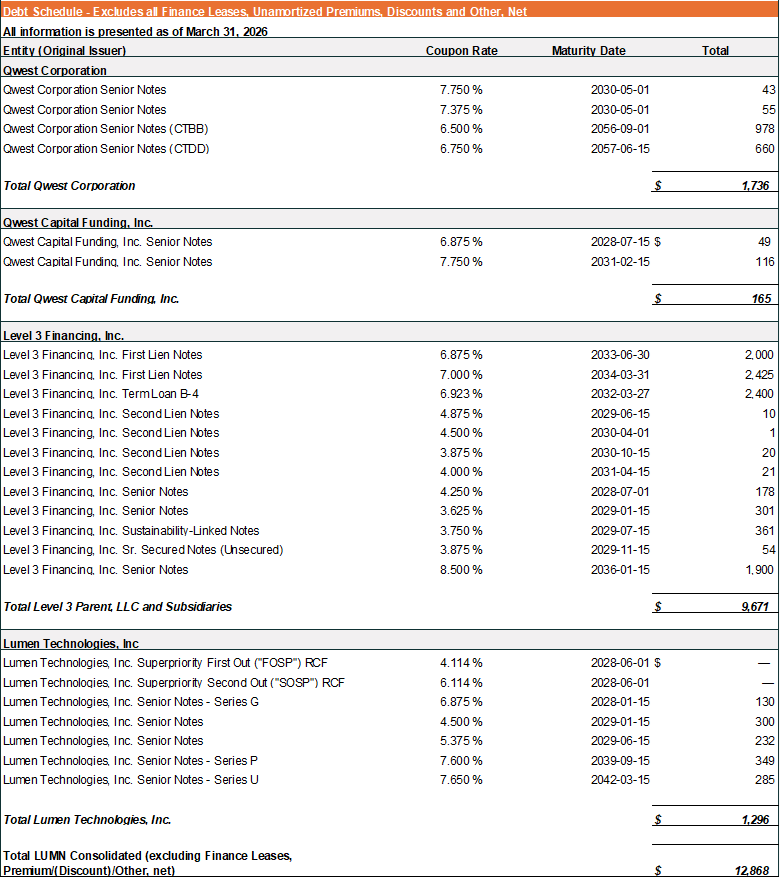

Debt Structure & Subsidiary Details – Level 3 growth has already inflected, a more unified/simpler capital structure should drive broader interest from investors.

Below shows Level 3’s revenue (from 10-K) and mix (Grow >60% of total), where revenue has already inflected positive. Post PCF/NaaS growth, Level 3 will be the vast majority of EBITDA in a few years (from current ~$1.9B LTM) as PCF + NaaS grows.

· Level 3 was bought for ~12x (similar to where Zayo was sold for) and represents the “crown jewel” assets (the intercity fiber network for AI/data centers/cloud that LUMN is aiming to turn into an AI infrastructure company). Level 3 is ~85% of “Grow” revenue.

· LUMN has continued to simplify the balance sheet/reporting. Recent debt exchanges have brought Qwest under the Lumen parent’s guarantee which aligns Qwest noteholders with Lumen and reduces the number of credit siloes/covenants.

Debt Structure Change post AT&T (recent refinancings further pushed maturities for Level 3 past 2030)

Source: Company Filings, LUMN investor presentations, S&P Global.

this is a wonderful report..Thanks for sharing..

any comment for $POET $CCOI ?

Interesting analysis! I'm curious how you're thinking about rising prices of energy, labor, construction, and key commodities like copper, all of which are driven by AI Capex. With the US AI infrastructure market increasingly consolidating around a stable oligopsony, do you see these factors putting downward pressure on LUMN margins?